How Bad Credit Can Affect Debt Consolidation Options

Bad credit can affect the types of debt consolidation options a borrower may be able to access, but it is usually not the only factor providers review. Income, current debt obligations, recent credit activity, and overall repayment capacity may also play a role when evaluating whether an option may be available.This page is designed to help borrowers better understand how bad credit may influence debt consolidation options, what additional factors may matter, and how to compare options more responsibly before taking the next step.

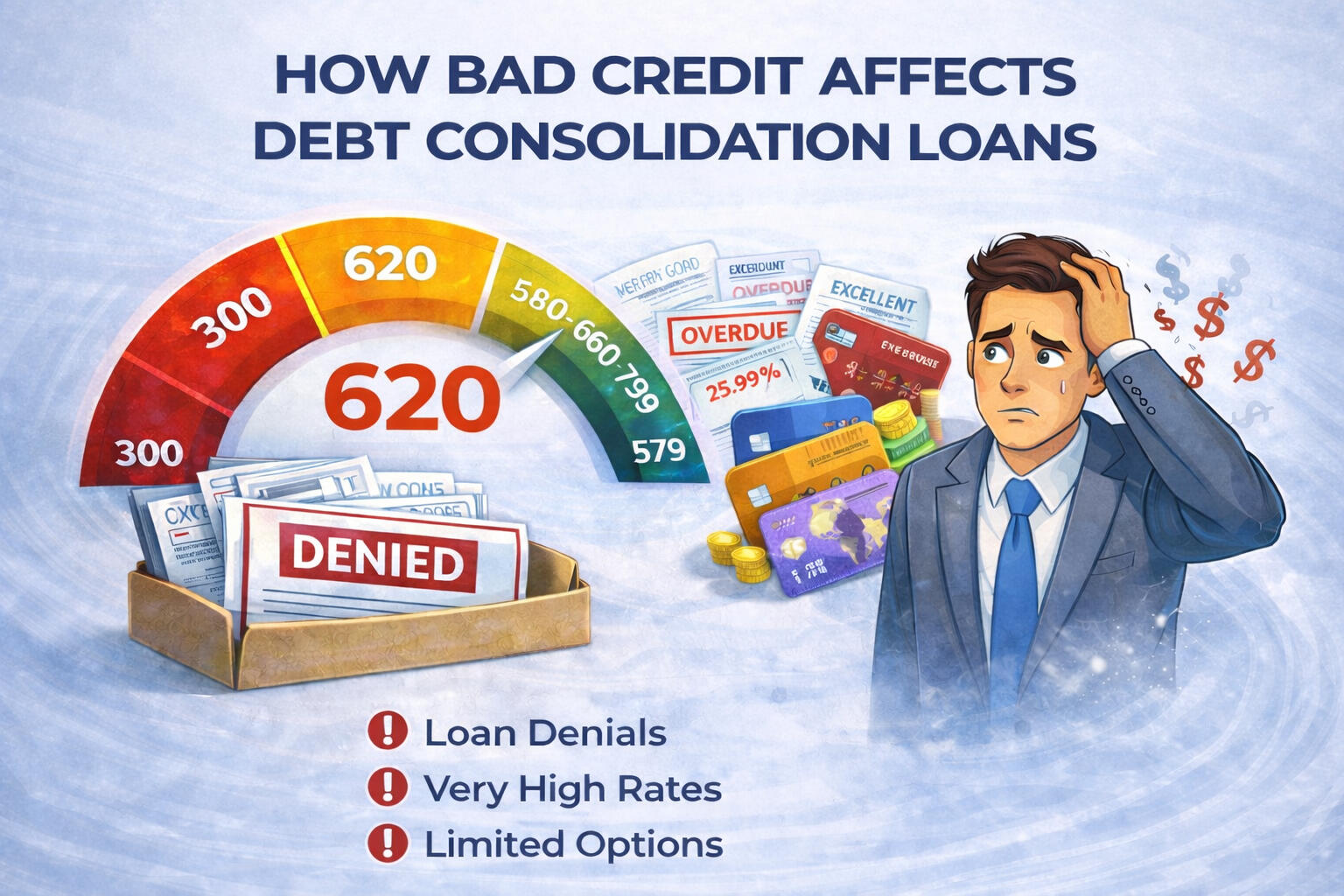

How Bad Credit Can Affect Debt Consolidation Options

Bad credit may affect debt consolidation in several ways, including the number of available options, the cost of borrowing, the loan amount offered, and the repayment terms presented. Some borrowers may still find options depending on their full financial profile, while others may encounter more limited choices or higher costs.A lower credit profile may lead to:-fewer available options

-higher APRs

-origination or other fees

-smaller approved loan amounts

-stricter qualification review

-less flexible repayment structuresThis does not automatically mean debt consolidation is unavailable, but it does mean that careful comparison and realistic budget review become more important.

What Providers May Review Besides Credit Score

Providers may look beyond credit score when evaluating debt consolidation options. Common review factors may include:-income consistency

-employment history

-current monthly debt obligations

-debt-to-income ratio

-recent delinquencies or negative marks

-recent credit inquiries

-requested loan amount

-overall repayment capacityTwo borrowers with similar credit profiles may still receive different outcomes depending on the rest of their financial picture. That is why it helps to review more than just credit score before comparing options.

What Terms and Costs Borrowers May Encounter

Borrowers with bad credit may want to prepare for the possibility of higher costs and more restrictive terms. Depending on the provider, some options may include:-higher APRs

-origination or administration fees

-smaller loan amounts

-shorter repayment periods in some cases

-less favorable monthly payment structuresBefore moving forward, it helps to compare:-APR

-monthly payment

-repayment term

-total repayment amount

-fees that may affect the true cost of borrowingA lower monthly payment may seem appealing, but longer repayment periods or added fees can increase the total amount paid over time.

When Debt Consolidation May or May Not Make Sense

Debt consolidation may make sense when a borrower is trying to simplify repayment, improve payment organization, or replace multiple balances with one structured payment that fits the budget.It may be worth reviewing when:-multiple debt payments are difficult to manage

-higher-interest balances are creating pressure

-one payment may improve repayment consistency

-the new payment is realistic and sustainableIt may be less helpful when:-the new loan adds unaffordable costs

-the repayment term greatly increases total repayment

-spending patterns remain unchanged

-the borrower is not yet in a position to support the new paymentThe key question is whether consolidation improves the situation in a realistic way, not just whether a new loan is available.

Alternatives to Consider

If suitable personal loan options are not available, it may make sense to consider other paths first. Depending on the situation, these may include:-focusing on debt reduction before reapplying

-reviewing hardship or payment options with current creditors

-improving income stability before comparing again

-exploring budgeting adjustments

-considering whether a smaller amount would be more realistic

-waiting to strengthen overall financial readinessIn some cases, preparation first may be more helpful than entering an option that increases long-term financial pressure.

How to Compare Options

Responsible comparison starts with understanding your current financial picture before reviewing any third-party option.Before comparing options, review:-your approximate credit score range

-your current income stability

-your monthly debt obligations

-the total amount of debt you are trying to consolidate

-whether your budget can support a new monthly paymentWhen comparing options, ask:-What is the APR?

-Are there origination or other fees?

-What is the total repayment amount?

-Is the monthly payment realistic?

-Does the repayment term help or hurt the total cost?

-Is this option solving the problem or delaying a bigger one?A more careful review process can help reduce the risk of choosing an option that creates more financial strain later.

Frequently Asked Questions

Can bad credit affect debt consolidation options?

Yes. Bad credit may affect approval standards, rates, fees, loan amounts, and the number of options available, though providers may also review other financial factors.Is credit score the only thing providers review?

No. Providers may also review income, employment consistency, current debt obligations, recent credit activity, requested amount, and repayment capacity.Will bad credit always mean higher borrowing costs?

Not every option will look the same, but lower credit profiles may be associated with higher costs or fewer available choices.Can debt consolidation still help if credit is low?

In some cases, yes. It depends on whether the option actually improves repayment structure, fits the budget, and reduces financial pressure in a sustainable way.What if suitable options are not available?

If suitable options are not available, it may help to focus on improving financial readiness, lowering debt pressure, or reviewing alternative paths before comparing again.

Ready to Compare Consolidation Options?

Explore debt consolidation options more responsibly based on your current profile and borrowing needs.

DisclaimerVETROS Financial Solutions LLC is not a lender, does not make credit decisions, and cannot guarantee loan approval or loan amounts. No application fee is charged. Loans are not available in all states. Short-term loans are not a long-term financial solution. Amounts and terms vary by lender and state.